Broadly speaking, the founding purpose of most endowment or foundation assets is to support a spending or distribution policy. Investment program success is commonly defined as an investment program’s capability to support this spending or distribution policy while preserving purchasing power and allowing for the modest growth of real wealth. With that said, how a spending policy or distribution policy is developed and defined can have a significant impact on an investment program’s ability to generate the returns necessary to support the above goal.

Here we outline why a spending rule is important, detail several commonly used policies, and consider the implications of different policies on both the investment portfolio and distribution outcomes.

Why Have a Spending Rule?

One reason to have a formal spending rule is to comply with the Uniform Prudent Management of Institutional Funds Act (UPMIFA), which has been adopted by many states and applies to the board of trustees or board of directors of the organization. UPMIFA was recently updated to include new language on how an organization’s board should prudently consider spending institutional funds, such as endowments.[1] The new language outlines seven guidelines for organizations to use when determining annual expenditures. In our opinion, it is prudent for nonprofit organization boards to implement a formal policy to address these guidelines. It should be noted that UPMIFA generally does not apply to funds held by a financial institution as a trustee, and further, funds held in a trust may be subject to additional spending limitations based on the terms of the trust and applicable state law.

Regardless of whether an organization follows the UPMIFA guidelines, our experience working with nonprofit organizations has shown us that having a firmly defined spending rule can help instill discipline into the budgeting and financial management process from an oversight perspective.

As an example, consider the difference between going into the grocery store with a budget in mind and a shopping list and going into the grocery store with no predetermined budget or list. In the former case, the outcome is fairly predictable and based on a disciplined process that typically results in spending what you intended and getting the items on your list.

Conversely, in the latter case, chances are you could spend more than you intended and leave with both unintended items and missing ones. Carrying the example over to a nonprofit organization, a spending rule can help define the budget (or at least the assets’ contribution to a budget) which, in turn, can help determine what operations, purchases, or other considerations can be added to the “shopping list.” This can help keep an organization from overspending in a given year, something that could potentially cause impairment to the purchasing power of the investment assets if they are used to cover the extra spending.

From an investment perspective, a spending rule can assist the board of directors and investment committee in determining the investment program’s required rate of return and risk tolerance objectives. For example, if the spending policy is set at 4%, and using 2% for long-term inflation and 0.5% for management and overhead fees, simple math would put the required rate of return at 6.5%. An investment manager could then use risk optimization to minimize risk against the return objective of 6.5%, allowing the portfolio to meet its investment goal efficiently and effectively. Without the orientation of the portfolio set on a required rate of return, the portfolio (specifically, the asset allocation) could be geared to return too much or too little. In the case of too much, a portfolio created with too high of a return target would be taking significantly more risk than required to meet the goal of 6.5%; in the case of too little, a portfolio created with too low of a return target would be taking less risk than is required to meet the goal of 6.5%, and consequently would likely fail to meet the return requirement.

In our view, the key takeaway from this is that setting a spending policy can help an organization determine an absolute benchmark to serve as a measurement of investment program success.

Given its importance to budgeting, financial management, and portfolio management, we recommend that a nonprofit entity clearly define a spending rule as part of the organization’s investment policy statement (IPS). We include a discussion of how to create a clearly defined spending rule as part of a nonprofit investment program in our white paper The Discipline to Succeed: Assembling a Robust Investment Policy Statement.

Implications of Spending Policies on Portfolio & Distribution Outcomes

In our experience, clients defer to five types of spending policies. There is no way to conclude if one policy is superior to any other policy on a general basis, since each has its merits in different situations. We believe the simple spending rule, for example, is perhaps the easiest to calculate and emphasizes current spending. The inflation-linked rule, while focusing on stability of spending, can become disassociated from the market value of the portfolio as a percentage if not recalculated at regular intervals. The rolling multiperiod average, geometric spending rule, and hybrid rule, on the other hand, while more complicated to calculate, can generally help stabilize spending as a dollar amount over the long term.

Five Types of Spending Policies

| Policy | Definition |

| Simple Spending Rate | Spending is equal to the specified spending rate multiplied by the beginning period market value. |

| Rolling Multiperiod Average, or UPMIFA | Spending is equal to the spending rate multiplied by an average of the market values of previous periods. This method reduces the volatility of required distributions from year to year. |

| Geometric Spending Rule | Spending in the current period is equal to a) the previous year's distribution adjusted for inflation times a smoothing rate (used to further reduce volatility, 0.7); plus b) the beginning market value of the portfolio times the spending rate and the residual of the smoothing rate (0.3 = 1 - 0.7). |

| Inflation-linked Rule | Begins with a set dollar amount, typically determined by a certain percentage of trailing market value, and the fixed amount is adjusted each year by an inflation index. |

| Hybrid Rule | Part of the annual spending amount is determined by an inflation adjustment of the previous year's spending, while the balance is determined by applying a fixed rate to the portfolio's market value. |

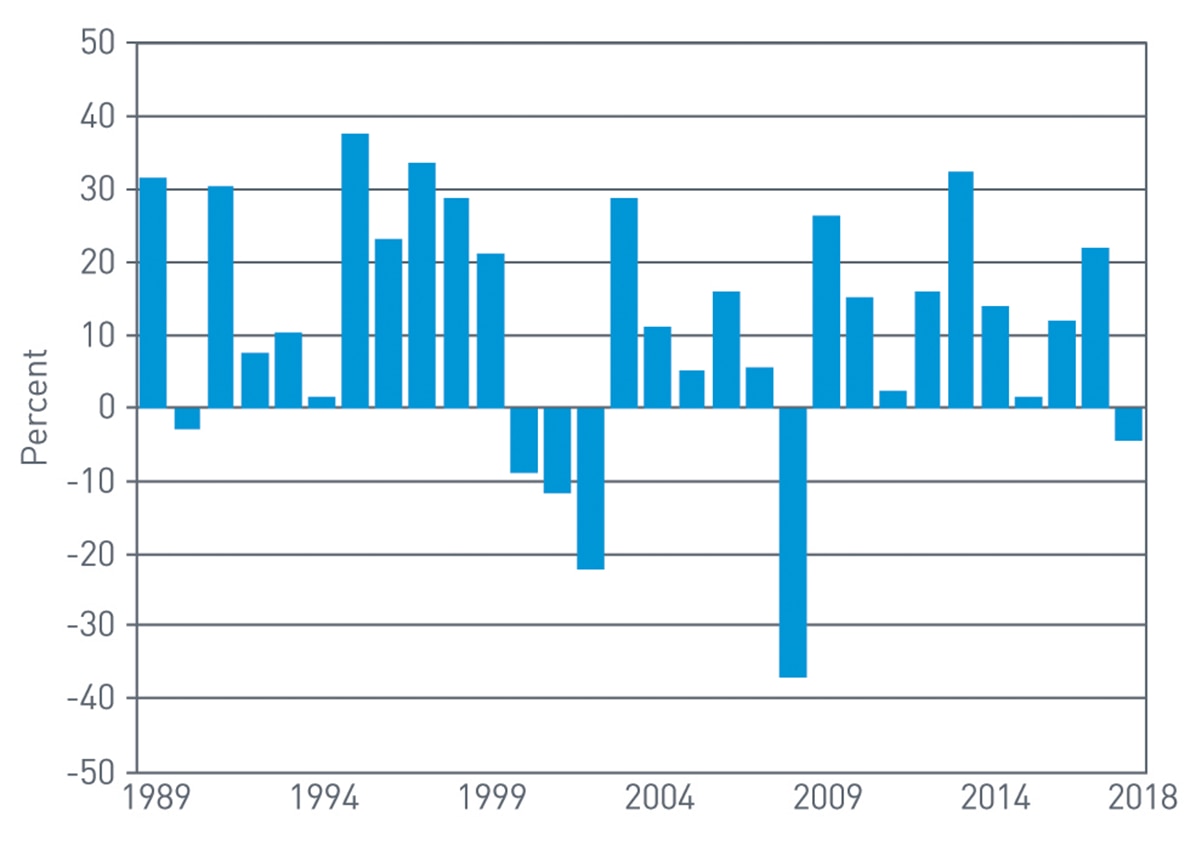

The charts below[2] illustrate how the different spending rules affect the amount of spending and the market value of the portfolio year over year. For simplicity, the portfolio was tracked against the S&P 500® from 1989–2019, and a base spending rate of 4.25% and long-term inflation rate of 2% are assumed. In the Portfolio Value chart, it is clear the inflation-linked rule resulted in the largest ending value, while the simple spending value ended in the lowest ending value. The reason for this discrepancy is seen in the Annual Spending chart, where annual spending is measured in dollars. Between 1989 and 1999, when the market moved significantly upward, the simple spending rate resulted in the largest increases in annual spending.

View accessible version of this chart.

Source: FactSet Research Systems Inc., PNC. As of 12/31/20,

View accessible version of this chart.

Source: FactSet Research Systems Inc., PNC. As of 12/31/20

Conversely, the inflation-linked rule resulted in significantly less, albeit stable, increases in annual spending. Because less spending leaves more funds in the portfolio to compound, the rule that results in less distributions (inflation) translates to greater portfolio ending value (over a period of generally positive returns) compared to a rule that results in greater distributions translating to a lower portfolio ending value. With regard to stability of spending, it is worth noting that the geometric-spending rule and inflation-linked rule resulted in the greatest stability of spending in dollar terms, while the hybrid rule and the simple spending rule resulted in the greatest stability of spending as a percentage of portfolio market value.

There are pros and cons to all five of the methods. While the simple spending rule is easy to understand, it can sometimes lead to volatile distributions.

The rolling three-year average spending rule can help reduce the volatility of distributions, but it might lead to an outsized distribution in years where the market value has declined significantly. The geometric spending rule can be complicated to calculate but reduces the volatility of distributions even further and, with a smoothing rule, can reduce the impact of a significant market decline on the annual distribution. The inflation-linked rule can result in stable distributions and can help the portfolio grow in value, but it can also cause the distribution to disconnect in relevancy as a percentage of the portfolio’s market value. Finally, the hybrid rule, while somewhat complicated to calculate, can lead to stable distributions in terms of dollar amounts and as a percentage of portfolio value.

View accessible version of this chart.

Source: FactSet Research Systems Inc., PNC. As of 12/31/20

Chart 4: Spending as Percentage of Beginning Portfolio Value

View accessible version of this chart.

Source: FactSet Research Systems Inc., PNC. As of 12/31/20

Conclusion

We have outlined the importance of clearly defining a spending or distribution policy, discussed five commonly used rules, and examined the pros and cons of those five rules. While it is impossible to identify any one rule as a singular best practice or panacea, we advise that a board of directors consider closely the pros and cons of each rule as it relates to the organization’s intention for the distribution.

We recommend working with your investment advisor or outsourced chief investment officer provider to understand fully the implications of the different rules on your organization’s portfolio and to confirm that, once developed, the spending policy is properly implemented as an input into the asset class allocation and portfolio construction process.

For more information, please contact your PNC Institutional Asset Management representative.

About Us

The Endowment & Foundation National Practice Group

The Endowment & Foundation National Practice Group builds on PNC Bank’s long-standing commitment to philanthropy and is focused on endowments, private and public foundations, and nonprofit organizations. We seek to help these organizations address their distinct investment, distribution and capital preservation challenges.

For more information, please contact Henri Cancio-Fitzgerald at henri.fitzgerald@pnc.com.

Accessible Version of Charts

| Year | Simple Rule | Rolling Rule | Geometric Rule | Inflation Rule | Hybrid Rule |

| 1990 | 100.00 | 100.00 | 100.00 | 100.00 |

100.00 |

| 1996 | 160.87 | 163.90 | 164.71 | 168.35 | 167.33 |

| 2002 |

253.40 | 263.71 | 271.63 | 311.33 | 275.84 |

| 2008 | 278.16 |

288.58 | 293.06 | 399.54 |

315.73 |

| 2014 | 308.16 |

317.49 |

315.33 |

514.18 | 364.24 |

| 2020 | 469.39 | 492.22 | 493.58 | 955.20 |

580.73 |

Chart 2: S&P 500 Annual Return

| Year | S&P 500 Annual Return |

| 1990 | -3% |

| 1996 | 23% |

| 2002 |

-22% |

| 2008 | -37% |

| 2014 | 14% |

| 2020 | 18% |

| Year | Simple Rule | Rolling Rule | Geometric Rule | Inflation Rule | Hybrid Rule |

| 1990 | 4.12 |

4.12 | 4.12 | 4.25 | 4.17 |

| 1996 | 8.41 |

7.09 |

6.84 | 4.79 | 7.05 |

| 2002 |

8.39 |

11.51 | 11.84 | 5.39 | 8.46 |

| 2008 | 7.45 |

11.04 | 11.45 | 6.07 |

8.48 |

| 2014 | 14.89 | 13.44 |

13.14 | 6.84 | 14.48 |

| 2020 | 23.62 |

21.26 |

20.61 |

7.70 |

23.79 |

Chart 4: Spending as a Percentage of Beginning Portfolio Value

| Year | Simple Rule | Rolling Rule | Geometric Rule | Inflation Rule | Hybrid Rule |

| 1990 | 4.3% | 4.3% | 4.3% | 4.4% | 4.2% |

| 1996 | 4.3% | 3.5% | 3.4% | 2.3% | 4.2% |

| 2002 |

4.3% | 5.6% | 5.6% | 2.2% | 3.1% |

| 2008 | 4.3% | 6.1% | 6.2% | 24% | 2.7% |

| 2014 | 4.3% | 3.7% | 3.7% | 1.2% | 4.0% |

| 2020 | 4.3% | 3.6% | 3.5% | 0.7% | 4.1% |